Five dealmaking trends detailing the dynamic, yet unwavering state of investing.

On any given day in the U.S., understanding the overall “health” of the private capital markets truly depends on who you ask. It’s increasingly important to have a keen eye towards the short-term bumps and hiccups that could become a major headache — and toward those situations that can be transformed into a competitive advantage.

In this article, we dive deep into Hamilton Lane Market Overview, highlights of which were recently presented during a keynote address at DealCloud Connect by Brian Gildea. In it, we’ll take a look at both what capital market trends are changing, and what trends remain a constant in the world of M&A.

What’s changing?

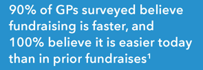

1. Fundraising is getting easier

What will surely be good news to those in fundraising and investor relations is: the time to secure capital and close a fund has decreased significantly. In fact, the average fundraising cycle in 2013 took over 15 months. As of early 2017, it took an average of 10 months.

One theory to explain this trend is that thanks to more connected, in-the-know investment community, LP due diligence cycles and conflict checks are faster and more efficient. A more likely cause for this trend, however, is that the overabundance of capital, combined with 50% less time spent (on average) to close a fund has made folks lazier.

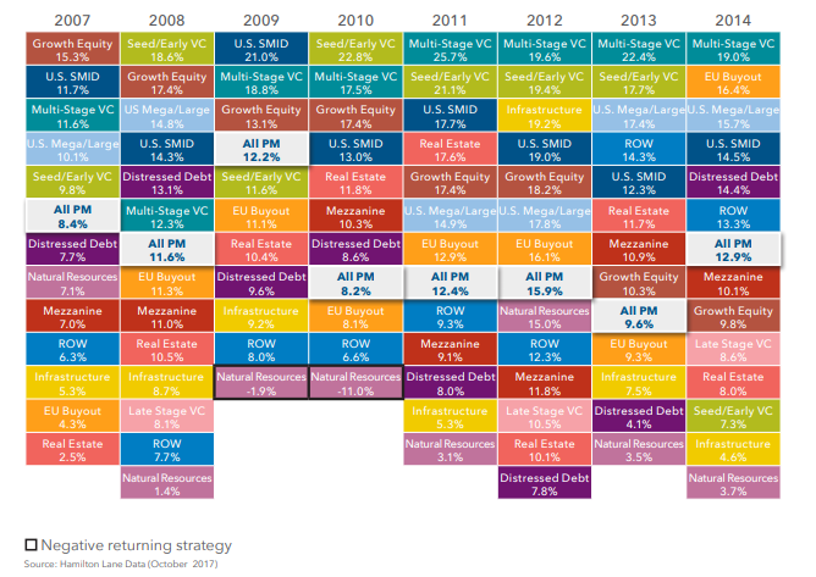

2. No vehicle is a clear winner

One key characteristic of an effective investor is the ability to pivot. Pivoting allows investors to avoid risk through a diversified portfolio by not hitching the proverbial wagon to just one horse.

A trend that’s emerging — and is clearly visible through The Periodic Table of Returns below — is that the top-performing asset classes are not consistent year-to-year. The same goes for the lowest performing asset classes. It’s evident that in picking multiple horses, the overall strategy matters — but so does the jockey. Fund managers need to be nimble, strategic and knowledgeable of all different types of investment vehicles. It’s clear from the data that without that aptitude, there’s money to be lost.

3. Private companies abound

According to Hamilton Lane, the “investable universe of private companies” is growing at unmatched pace (180% since 2011). Comparatively, the number of U.S. private equity-backed companies has grown by 42%, and the number of private markets net asset value (NAV) has grown by 29% in the same time period. This growth in volume of privately held companies should spur a frothy mergers and acquisitions market in the years to come.

What’s staying the same?

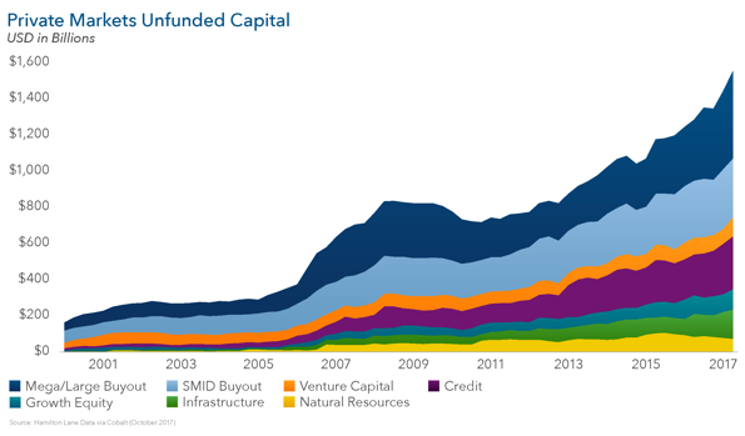

4. Dry powder

The more private equity firms raise, the more that money sits idle. This “dry capital” phenomenon illustrated in the graph below shows that across every type of investment vehicle, asset managers have not been able to properly put money to work.

In fact, these “capital overhang” numbers have grown quite steadily since 2007, with no capital being hastily deployed into a specific investment vehicle. What does this mean for the M&A community at large? Hamilton Lane suggests this is “a sign of a healthy, vibrant market well-integrated into global economic flows.”

5. The public vs. private equity debate

When you pit the public and private markets against each other, mixing market data and overall sentiment together is the only way to decide on your allocation balance.

On one hand, private equity has generated 12.3% returns on average over the past 20 years, clearly outperforming its public market equivalents (PMEs). On the other hand, these same firms have collected an average fee of 7%.

Despite all of these exciting advantages, in some ways the private markets are still peanuts compared to the world’s largest publicly traded companies. As Hamilton Lane explains, “all of the projected contributions in 2017 wouldn’t be enough to buy all of Apple’s stock.” In our estimation, this “Main Street” versus “Wall Street” fight will continue at the same pace, and with the same outcome that has been observed over the last decade: every firm will allocate funds into both and find a healthy mix between the two.

To learn more about the ways leading investment firms are using data to stay abreast of these trends and respond intelligently to the market’s twists and turns, click here.